Equal Housing Lender. Bank NMLS #381076. Member FDIC.

Equal Housing Lender. Bank NMLS #381076. Member FDIC.

Wilmington Trust Newsroom

Press Releases

The latest news from Wilmington Trust.

The outlook focuses on three main themes: the U.S. economy, income inequality, and emerging markets opportunity.

WILMINGTON, DEL—Wilmington Trust has released its annual Capital Markets Forecast titled “Uncharted Waters: Will Political Riptides Threaten Portfolio Returns?” The outlook from Wilmington Trust’s investment team focuses on three main themes: the U.S. economy, income inequality, and emerging markets opportunity.

“The election of Donald Trump as president of the United States has proved a boon to the markets, but can the rally be sustained?” said Tony Roth, chief investment officer for Wilmington Trust. “Risk, uncertainty, and slow growth persist, but President Trump’s growth-stimulating policies could boost the economy in the short-term. However, the long-term impact of those stimulus programs on national debt keeps our investment team up at night.

“Lack of sleep notwithstanding, we’re fairly optimistic about 2017. Our advice to investors is to stay nimble and be prepared to pounce on opportunities and steer clear of hazards as we continue to navigate economic chop.”

U.S. Economy Pulling Ahead—But Risks Persist

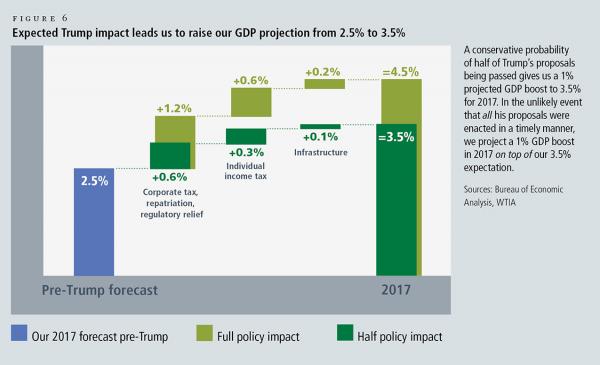

The U.S. economy stands at a crossroads. Entering the eighth year of tepid economic recovery, it remains to be seen if President Trump’s pro-growth programs, promised during the campaign, will come to fruition. Key economic proposals include lowering income taxes, eliminating estate and corporate alternative minimum taxes, repatriating corporate earnings, increasing trade restrictions, and reducing business regulations.

Despite the Republicans’ bicameral majority in Congress and control of the executive branch, their fiscal conservative nature may water down the proposals that do come to fruition. Still some stimulative policy changes are likely to be enacted, which will positively affect the labor market, wages, and consumer spending. Additionally, American companies would benefit from a lower corporate tax rate and a simpler tax system.

Wilmington Trust is optimistic for the U.S. economy, but longer-term concerns include a shrinking labor force due to lower birth rates, as well as the mounting federal deficit. Debt as a share of gross domestic product has already doubled (from 35% to 74%) since the recession and is projected to rise to 86 percent in 10 years according to the Congressional Budget Office. If President Trump’s near-term pro-growth policies are deficit-financed, the debt problem will be exacerbated.

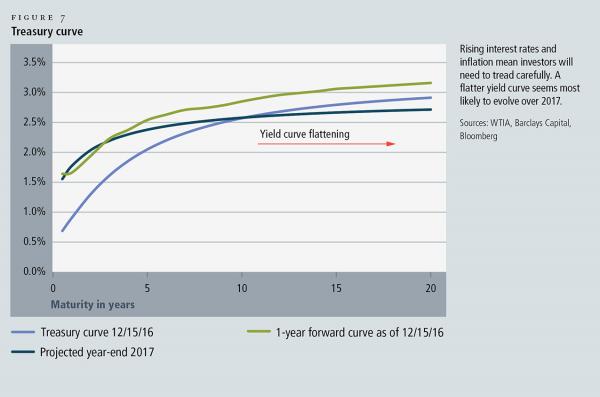

President Trump’s fiscal policies carry inflationary risks, which could lead the Federal Reserve to quicken the frequency of interest rate hikes. While not the base case scenario, this series of events could, ironically, reverse economic recovery.

Income Equality—Finding the Yield Sweet Spot

Despite stronger near-term economic growth, investors remain stuck in a slow-growth, low-return environment. Coupled with sharply rising market rates, this creates peril within income-oriented asset classes, which could drop in value. A flatter yield curve seems likely to evolve in 2017. Investors will need to plan carefully to boost portfolio returns to deal with a one-two punch of rising interest rates and inflation.

Rising inflation bodes well for Treasure inflation-protected securities (TIPS). Wilmington Trust’s preference is for shorter-duration TIPS, as a longer term increases the risk of interest rate movements. Additionally, rising interest rates could prove difficult for taxable and tax-exempt investment-grade markets, as their lower yield levels provide little protection against diminishing principal values.

On the stock front, dividend-thirsty investors have pushed up market prices to a level that is now vulnerable to significant price depreciation in the face of rising interest rates. Especially susceptible are rate-sensitive utilities and consumer staples sectors, which have underperformed since the election. In contrast, the earnings recession now appears to be in the rearview mirror, and Wilmington Trust expects solidly higher earnings in 2017.

International stock markets might be another place where income plays a bigger role in total return. With growth rates in Europe and Japan likely to remain challenged in the year ahead, price gains in stocks should be somewhat limited. These markets do generally provide greater dividend yields than U.S. stocks, and with their relative cheapness, they remain reasonably attractive.

Emerging Markets—Opportunity on the Doorstep

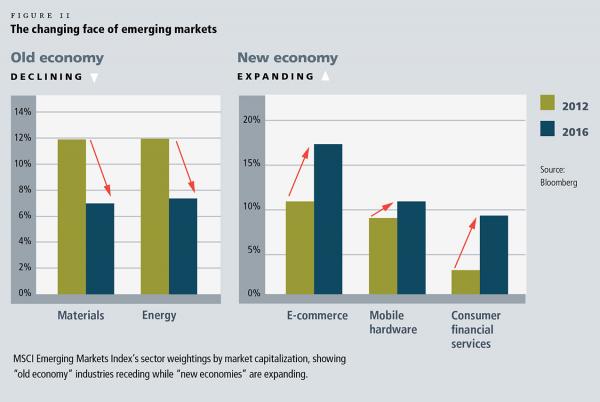

In emerging markets, a sustained expansion of the purchasing power of middle-class consumers continues. This is particularly evident in Asian economies, especially China and India. This presents many opportunities for emerging markets companies as consumer demand for their products and services surges.

“Old economy” heavy industries that focused on metals, oil and gas, chemicals, power production and the like, are receding at a pace faster than Wilmington Trust predicted in last year’s forecast. Inversely, “New economy” industries are experiencing rapid growth as we predicted last year. The majority of new economy companies, like e-commerce, mobile hardware, and consumer financial services, are less dependent on infrastructure and less sensitive to commodity volatility,

The pace of emerging markets growth gained momentum in 2016, due in part to commodity prices leveling off, the Fed’s decision to slowly raise rates, and improved political stability. Emerging markets initially reacted negatively to the U.S. election outcome, but the slump was not severe, and in certain respects, improved buying opportunities. Despite fears over a trade war and a strong U.S. dollar, Wilmington Trust doesn’t believe the emerging markets space will be hindered by those influences.

China has restored some calm to its domestic stock and currency markets, and stimulated its economy by boosting the expansion of business credit, enabling growth toward the end of 2016. Sino-U.S. trade, however, faces a real threat from President Trump’s proposed trade policies, such as a 45-percent tariff on Chinese imports. Pain would be shared by both two countries since China is the largest source of U.S. imports and the third-largest recipient of American exports. U.S. consumers could expect to pay higher prices for goods as an outcome of a trade war with China.

More economic insights can be found in Wilmington Trust’s 2017 Capital Markets Forecast commentary, as well as related videos and materials at WilmingtonTrust.com/CMF.